Financial institutions globally face an unprecedented surge in sophisticated identity fraud fueled by automated tools available on encrypted messaging platforms. The rapid democratization of artificial intelligence technologies allows illicit actors to compromise traditional identity verification pipelines with minimal technical expertise. Automated programs now circulating on communication networks offer specialized services designed specifically to circumvent customer onboarding protections, presentation attack detection systems, and biometric authentication protocols. Regulated entities must urgently evaluate their defense architectures to counter these industrial-scale verification threats. As legacy biometric barriers become increasingly obsolete, compliance frameworks require a fundamental shift toward multi-layered behavioral and cryptographic verification strategies.

Table of Contents

Scalable Synthetic Identity Generation and Automated Biometric Deception

Criminal networks are rapidly deploying specialized software solutions to automate the fabrication of high-quality identity documents and synthetic biometric traits. These software utilities manipulate digital imagery, modify metadata, and overlay synthetic faces onto existing document templates to construct convincing fraudulent credentials. The structural integrity of these digital counterfeits often satisfies standard automated document validation checks, allowing bad actors to clear the initial stages of remote customer onboarding seamlessly. Beyond document forgery, the integration of advanced neural networks enables the creation of dynamic biometric samples that mimic human behavioral patterns during live verification sessions.

The proliferation of these automated forgery mechanisms represents a structural shift in the financial crime landscape. Previously, executing high-fidelity document forgery required specialized graphic design skills and access to sophisticated printing equipment. Today, readily accessible digital suites generate customized, high-resolution identity documents within minutes based on simple text inputs provided by illicit operators. This industrialization of forgery removes the traditional cost barriers associated with identity fraud, enabling single threat actors to launch coordinated, concurrent registration campaigns across dozens of regulated financial entities simultaneously.

As financial platforms increasingly rely on digital identification frameworks, the financial sector has seen an exponential rise in synthetic document alterations. Sophisticated fraud rings exploit variations in automated document validation algorithms, systematically testing templates against different onboarding workflows to identify specific vulnerabilities. By altering thin layers of data on legitimate credentials, such as modifying dates of birth, identification numbers, or portrait photographs, attackers create entirely new credit profiles. These synthetic profiles slowly build positive financial histories, laying the groundwork for substantial future financial losses when the accounts are eventually abandoned or liquidated.

The Rise of Virtual Camera Attacks and Presentation Security Failure

Beyond static document manipulation, contemporary threat actors utilize sophisticated video injection methodologies to undermine real-time biometric validation mechanisms. Virtual camera infrastructure allows fraudsters to bypass physical optical sensors entirely, feeding pre-recorded or artificially generated video streams directly into the browser or mobile application interface during active verification prompts. This technique invalidates the assumption that a live user is physically interacting with an authorized device camera. Consequently, standard facial recognition systems frequently authenticate these synthetic injections as legitimate human presence, failing to detect the artificial nature of the digital input.

The escalation of virtual camera methodologies represents an existential threat to remote identity verification paradigms globally. Fraud networks continuously refine injection techniques, utilizing customized browser extensions and emulated operating systems to hide the presence of virtual video drivers from application security tools. By mimicking the hardware signatures of standard mobile devices, these malicious setups ensure that the incoming video feed appears completely genuine to the underlying security software. The success of these presentation attacks demonstrates that traditional facial matching algorithms are no longer sufficient when operating in isolation from deeper device and network analysis.

The structural impact of these biometric delivery exploits is evident in the massive surge of native virtual camera actions documented across international compliance frameworks. Fraud syndicates systematically share operational configurations, optimizing video frame rates, resolution dynamics, and illumination characteristics to match the strict operational tolerances of specific biometric software engines. This collaborative refinement allows attackers to achieve high success rates when targeting prominent financial service providers, virtual asset exchanges, and electronic payment processors. The ability to neutralize live biometric checks at scale undermines a core foundation of modern digital customer onboarding security.

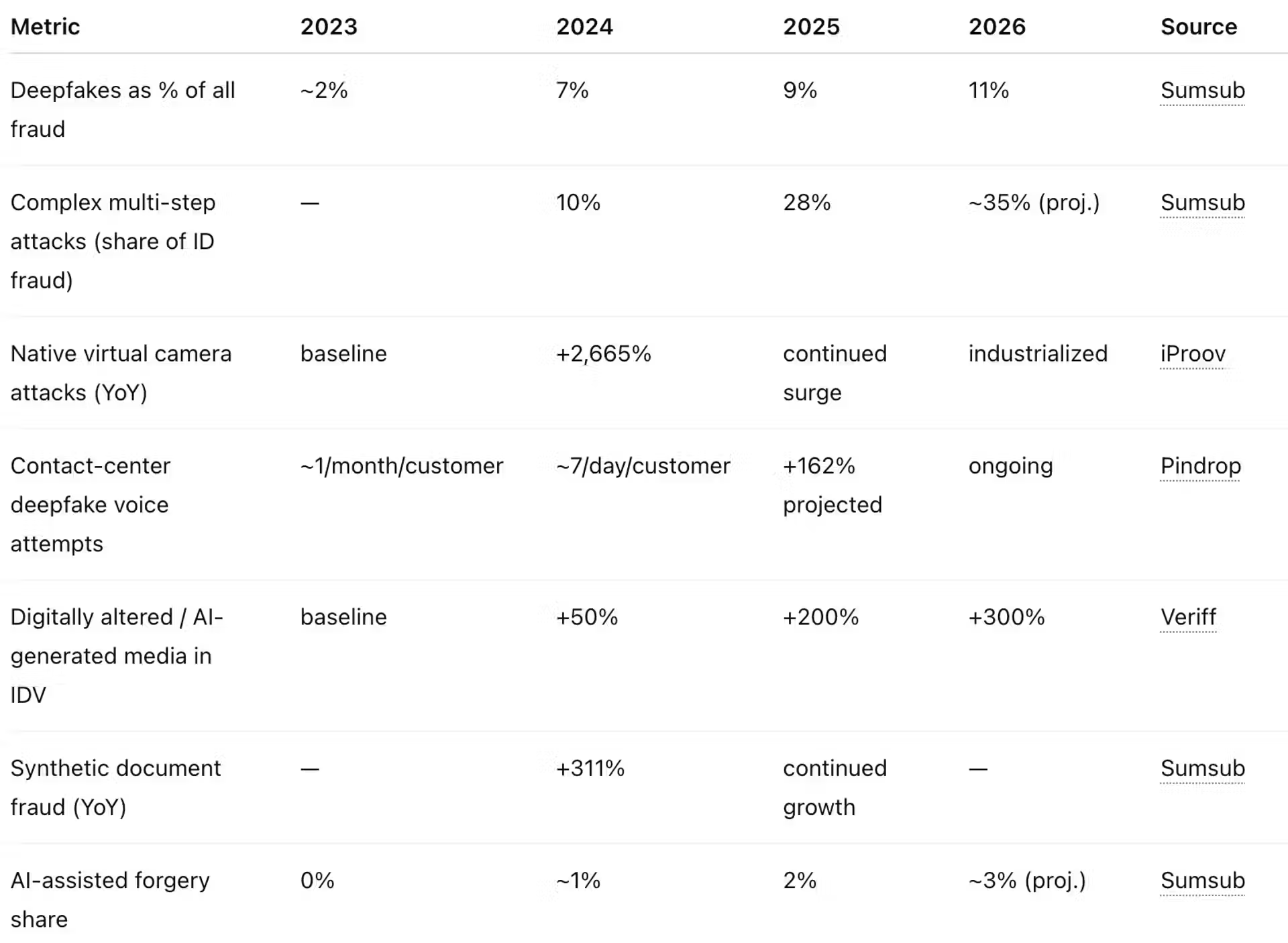

Here is the analytical data reflecting the metric changes across recent verification cycles:

Data from Tech-Insider

Industrialized Deepfake Voice Operations and Comprehensive Defense Restructuring

The threat landscape expands further with the deployment of industrialized deepfake voice technology targeting telephonic communication channels and remote verification hotlines. Malicious actors employ real-time voice cloning software to impersonate account holders, bypass telephonic biometric barriers, and manipulate customer service representatives during high-value transactional authorizations. These voice synthesis models analyze short audio samples of target individuals to replicate speech patterns, intonations, and linguistic habits with striking precision. This development compromises the security of telephone banking systems, enabling unauthorized fund transfers, account takeovers, and sensitive data extraction.

To mitigate these complex multi-step attack vectors, corporate compliance infrastructures must move beyond isolated verification points and embrace comprehensive, continuous monitoring protocols. Financial institutions can no longer depend solely on the initial onboarding event to guarantee the enduring legitimacy of an account profile. Defense systems must integrate contextual data analysis, including real-time evaluation of device hardware configurations, behavioral anomalies, and payment pattern deviations. Combining cryptographic identity verification with strict behavioral tracking establishes a resilient defense capable of detecting fraudulent activity even after initial biometric perimeters are breached.

Organizations must also implement advanced detection layers capable of identifying the subtle artifacts left behind by generative artificial intelligence models and video injection software. This involves deploying deep fake detection systems that scrutinize media files for structural inconsistencies, irregular lighting patterns, and unnatural pixel distributions. Furthermore, compliance teams must establish rapid response protocols to neutralize accounts immediately when behavioral indicators signal automated control or synthetic ownership. Continuous technological updates and rigorous testing against emerging exploitation frameworks remain vital to maintaining institutional integrity against advancing synthetic identity networks.

AML Typologies for Identity Verification Deception

Compliance personnel must actively monitor and identify operational patterns associated with automated identity circumvention and synthetic document deployment. Recognizing these indicators early allows institutions to prevent systemic account exploitation.

- Automated Metadata Discrepancy: Digital identity documents exhibit identical creation timestamps, sequential serial numbers, or recurring software signatures across separate customer profiles.

- Virtual Device Emulation: Onboarding sessions originate from identical device hardware configurations, utilizing customized operating system versions frequently associated with software emulators.

- Inconsistent Biometric Behavior: Facial recognition video feeds demonstrate a complete absence of natural micro expressions, abnormal pupillary responses, or unnatural edge distortions along the facial perimeter.

- Repeated Audio Patterns: Telephonic interactions feature subtle acoustic loops, synthetic voice textures, or sudden changes in background noise profiles during identity authentication phases.

- Coordinated Registration Clusters: Multiple accounts are established within a brief timeframe using disparate personal data points that nonetheless share identical IP addresses or device profiles.

- Document Template Reuse: Distinct applicant profiles submit identity cards featuring identical background textures, ambient lighting artifacts, or physical wear marks.

Key Points

- Remote identity verification pipelines face escalating vulnerabilities due to the widespread availability of automated bypass tools on encrypted networks.

- Virtual camera injections neutralize standard live biometric checks by feeding synthetic media directly into application interfaces.

- Synthetic identity creation has reached an industrial scale, combining genuine data with artificial fabrications to deceive automated validation tools.

- Advanced voice cloning software targets telephonic banking infrastructures, facilitating unauthorized account access and corporate manipulation.

- Holistic compliance frameworks must incorporate continuous behavioral monitoring and deep hardware analysis to counter synthetic identity fraud.

Related Links

- Financial Action Task Force Guidance on Digital Identity

- European Banking Authority Report on Remote Onboarding Solutions

- Financial Crimes Enforcement Network Advisory on Cybercrime Risks

- Egmont Group Risk Assessment on Synthetic Identity Laundering

- Federal Reserve Information on Synthetic Identity Fraud Mitigation

Other FinCrime Central Articles About Fake Digital IDs

- Dutch Police Seize Assets and Arrest Eight in Fake Digital ID Case

- Italy Dismantles Romance Scam-Related Money Laundering Network

- Digital Identification Risks in the Era of Deepfake Technology

Source: Tech Insider, by Nadia Dubois

Some of FinCrime Central’s articles may have been enriched or edited with the help of AI tools. It may contain unintentional errors.

Want to promote your brand, or need some help selecting the right solution or the right advisory firm? Email us at info@fincrimecentral.com; we probably have the right contact for you.