Trulioo’s newly unveiled digital trust framework marks a decisive shift in how financial institutions approach anti-money laundering and fraud prevention. While traditional identity verification has long been the first barrier against illicit activity, this evolution turns compliance into a continuous intelligence cycle rather than a static onboarding event. By embedding real-time verification, biometric recognition, and ongoing Know Your Business (KYB) risk monitoring into a single ecosystem, Trulioo positions itself at the center of a rapidly changing regulatory landscape where the integrity of digital identity underpins AML effectiveness.

Table of Contents

Transforming AML Compliance Through Digital Identity Intelligence

The company’s latest announcement at Money20/20 USA signals a move from verification to vigilance. Instead of treating compliance as a check-the-box process, Trulioo’s end-to-end model continuously evaluates customer behavior, ownership dynamics, and transactional anomalies. Such advancements directly target a critical pain point for regulated entities: the fragmentation between KYC onboarding and ongoing due diligence. The seamless connection of these two domains closes the gaps that criminal actors often exploit to move illicit funds through digital channels.

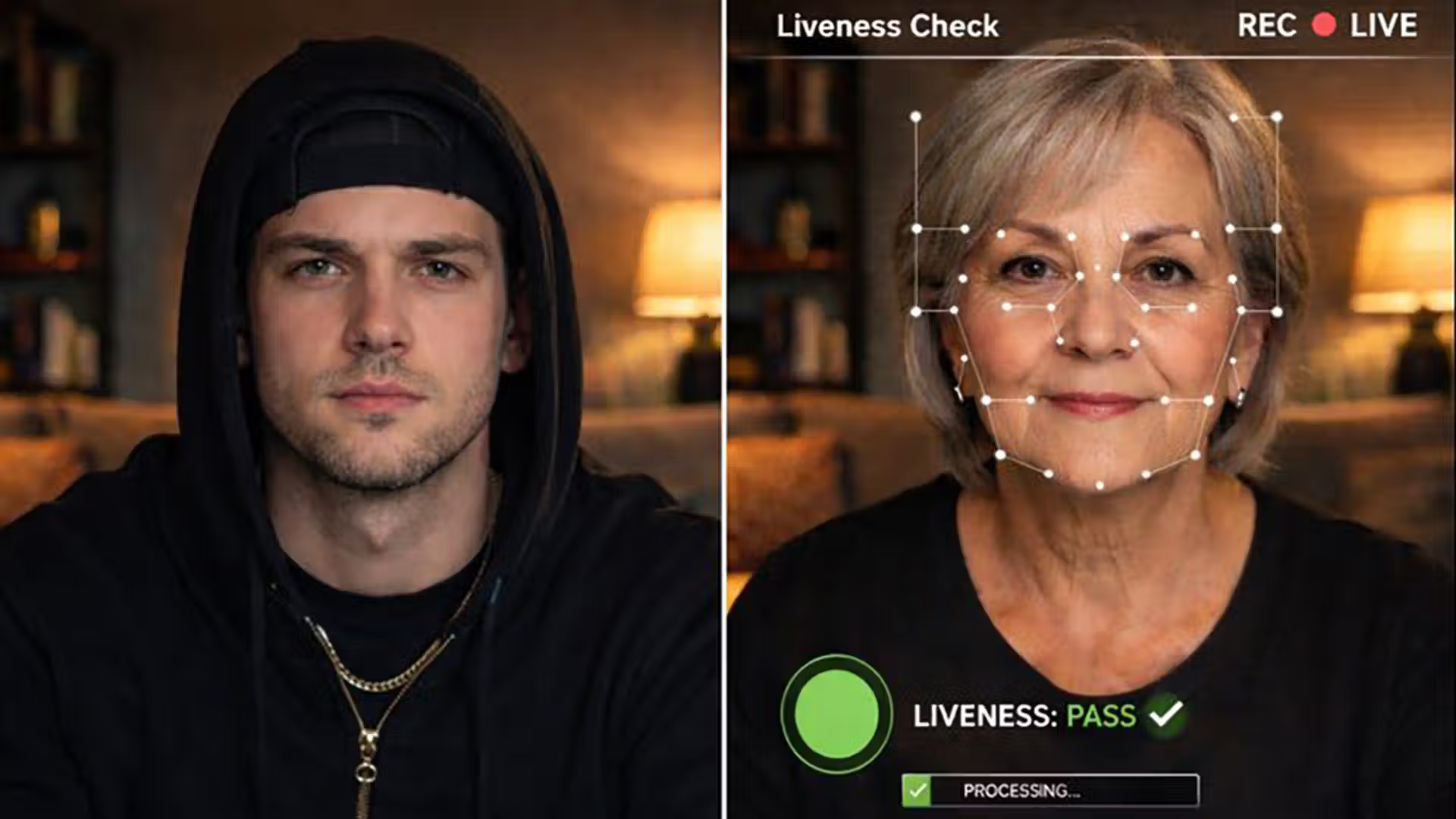

Trulioo’s expanded biometric capabilities introduce an additional layer of AML resilience. Known-face recognition systems, now capable of one-to-many facial comparisons, can identify repeat fraudsters even when they attempt to use new identities. This form of behavioral biometrics, when combined with document integrity checks, strengthens defense mechanisms against identity layering, a common laundering technique where multiple synthetic identities are cycled through online platforms to legitimize funds.

The system’s foundation on AI-driven analytics allows for dynamic adaptation to emerging typologies. By integrating more than sixty fraud-identifying signals, Trulioo’s redesigned customer portal converts static KYC processes into data-driven intelligence hubs. This shift supports regulated institutions under the EU’s evolving AMLA framework and the FATF’s emphasis on beneficial ownership transparency. Each verification or business profile update feeds a broader network of risk indicators, producing what Trulioo calls a “continuous digital trust lifecycle.” The outcome is a more proactive stance in detecting cross-border laundering networks before they fully manifest within financial systems.

The Rise of Continuous KYB and Dynamic Business Risk Profiling

A particularly transformative component of Trulioo’s platform lies in its redefinition of KYB. Traditionally, corporate due diligence has focused on static registry data, which quickly becomes obsolete when companies restructure, change ownership, or move operations across jurisdictions. Trulioo’s continuous KYB framework aims to address this deficiency by tracking legal entity evolution in real time.

Through automated monitoring, the platform flags changes in company status, beneficial ownership, or regulatory filings, triggering alerts that prompt compliance teams to reassess exposure. This is especially relevant in light of recent regulatory demands emphasizing ultimate beneficial owner (UBO) transparency and enhanced scrutiny of shell companies. The integration of sanctions and adverse media signals allows financial institutions to preemptively mitigate exposure to sanctioned entities or politically connected intermediaries.

The inclusion of web and social analytics within the KYB engine represents a major step forward for AML risk intelligence. Trulioo’s algorithms assess a company’s digital footprint, comparing its declared activity with its actual online presence. This approach helps identify inconsistencies that might point to concealment strategies, proxy operations, or shadow ownership networks. For example, a company registered as an agricultural exporter but with an active digital advertising profile related to cryptocurrency exchanges would raise automated red flags. Such correlation-based intelligence helps compliance teams focus investigative efforts where discrepancies are most likely to signal laundering behavior.

Business risk and reputation scoring further extend this paradigm. By synthesizing registry data, behavioral indicators, and network associations, Trulioo generates composite risk evaluations that evolve as new data surfaces. This continuous recalibration prevents the “risk freeze” that often occurs when institutions rely solely on periodic reviews. For multinational banks managing thousands of corporate clients, this adaptive scoring is particularly valuable, enabling proactive remediation and minimizing the window of exposure to financial crime.

From an AML perspective, continuous KYB reduces dependency on manual review cycles and outdated data pulls. Automated workflows ensure that remediation steps are initiated as soon as anomalies appear, aligning compliance performance with regulatory expectations of “timely and proportionate response.” The model anticipates the regulatory trajectory where real-time risk assessment will become mandatory, not optional, across both financial and non-financial obliged entities.

Integrating Biometric Defenses Into the AML Lifecycle

One of the most critical challenges in financial crime prevention is identity fraud that evolves faster than verification methods. Trulioo’s latest biometric authentication suite addresses this by embedding AI-driven face matching within the core of digital onboarding and monitoring. The technology’s ability to detect repeat fraudsters across multiple platforms closes a loophole frequently exploited in layering and integration phases of money laundering.

The “known faces” feature expands verification into behavioral analysis. Each face captured during a verification attempt is matched not only against identity documents but also against a repository of historical facial data linked to confirmed users. When an attempt is made using similar attributes to a previously flagged individual, the system instantly signals high-risk behavior. This has resulted in double-digit reductions in manual review volumes among early adopters, showing measurable operational efficiency without compromising compliance accuracy.

Beyond facial recognition, Trulioo’s tamper-detection system for non-ID documents introduces a much-needed safeguard for secondary verification materials such as utility bills and bank statements. Fraudulent document submission is a recurring method in illicit finance, particularly during address verification or proof-of-income checks. By applying AI-based pattern recognition to detect irregularities in file structure, image compression, and metadata, Trulioo’s technology minimizes acceptance of manipulated documents.

For AML teams, these layered defenses translate to fewer false positives and stronger evidence chains when reporting suspicious activity. The system’s ability to differentiate between legitimate anomalies and structured deception enhances case-building for regulatory reporting. When combined with a redesigned API and SDK that promote low-friction user experiences, the platform resolves a long-standing conflict between customer satisfaction and compliance rigor. The net effect is a measurable improvement in fraud prevention and user retention simultaneously, a combination rarely achieved in AML system design.

Building a Trust-Centric Ecosystem for AML Enforcement

Trust has become the operational currency of modern financial systems. Yet building trust in the digital domain requires transparent identity infrastructures capable of withstanding global regulatory scrutiny. Trulioo’s platform acts as both an intelligence engine and a compliance control tower, aligning real-time data analytics with evolving AML standards.

Its risk intelligence fabric integrates external signals with internal transaction histories, establishing a closed feedback loop between fraud detection and compliance validation. When a business undergoes a structural change, such as a shareholder transfer or jurisdictional move, that update cascades instantly across verification layers. This continuous synchronization prevents outdated or incomplete data from undermining AML risk assessments.

The broader implication extends beyond operational efficiency. As global regulators push toward interoperable identity frameworks and cross-border data exchange, solutions like Trulioo’s position themselves as neutral infrastructure layers for trust verification. This could pave the way for more harmonized enforcement across jurisdictions, addressing the fragmentation that currently enables transnational laundering schemes.

For enterprises, the ability to align AML monitoring, biometric verification, and KYB risk scoring within a single interface eliminates the silo effect. It allows compliance officers to visualize exposure across both individual and corporate dimensions, streamlining Suspicious Activity Report preparation and improving collaboration between fraud and compliance departments. Over time, such systemic visibility could redefine regulatory expectations for effectiveness, shifting emphasis from procedural compliance toward demonstrable risk mitigation outcomes.

Trulioo’s approach also anticipates the rise of AI-governed regulatory audits. As supervisory bodies adopt data-driven inspection models, platforms capable of providing transparent, auditable verification logs will hold strategic value. Every verification event within Trulioo’s ecosystem can be replayed, audited, and validated, ensuring traceability consistent with FATF recommendations on technology-assisted due diligence. The convergence of AI governance and AML enforcement thus transforms identity management into a compliance instrument rather than a customer onboarding accessory.

Related Links

- Financial Action Task Force (FATF)

- FINTRAC (Financial Transactions and Reports Analysis Center of Canada)

- FinCEN (Financial Crimes Enforcement Network)

- European Banking Authority (EBA)

- Bank for International Settlements (BIS)

Source: Trulioo

You can find Trulioo’s page in the FinCrime Central AML Solution Provider Directory here.

Want to know which solutions can be envisaged for your specific needs?

Access the full feature-based AML Solution Provider Directory here

Some of FinCrime Central’s articles may have been enriched or edited with the help of AI tools. It may contain unintentional errors.

Want to promote your brand with us or need some help selecting the right solution or the right advisory firm? Email us at info@fincrimecentral.com; we probably have the right contact for you.